When financing a vehicle, one of the most important decisions you’ll make is choosing between a fixed or variable interest rate. This choice affects more than just your monthly payment. It influences your total interest costs, your ability to budget, and how much financial risk you carry throughout the loan term.

Understanding how each rate type works can help you align your financing with your goals, whether you’re looking for predictability, flexibility, or short-term savings.

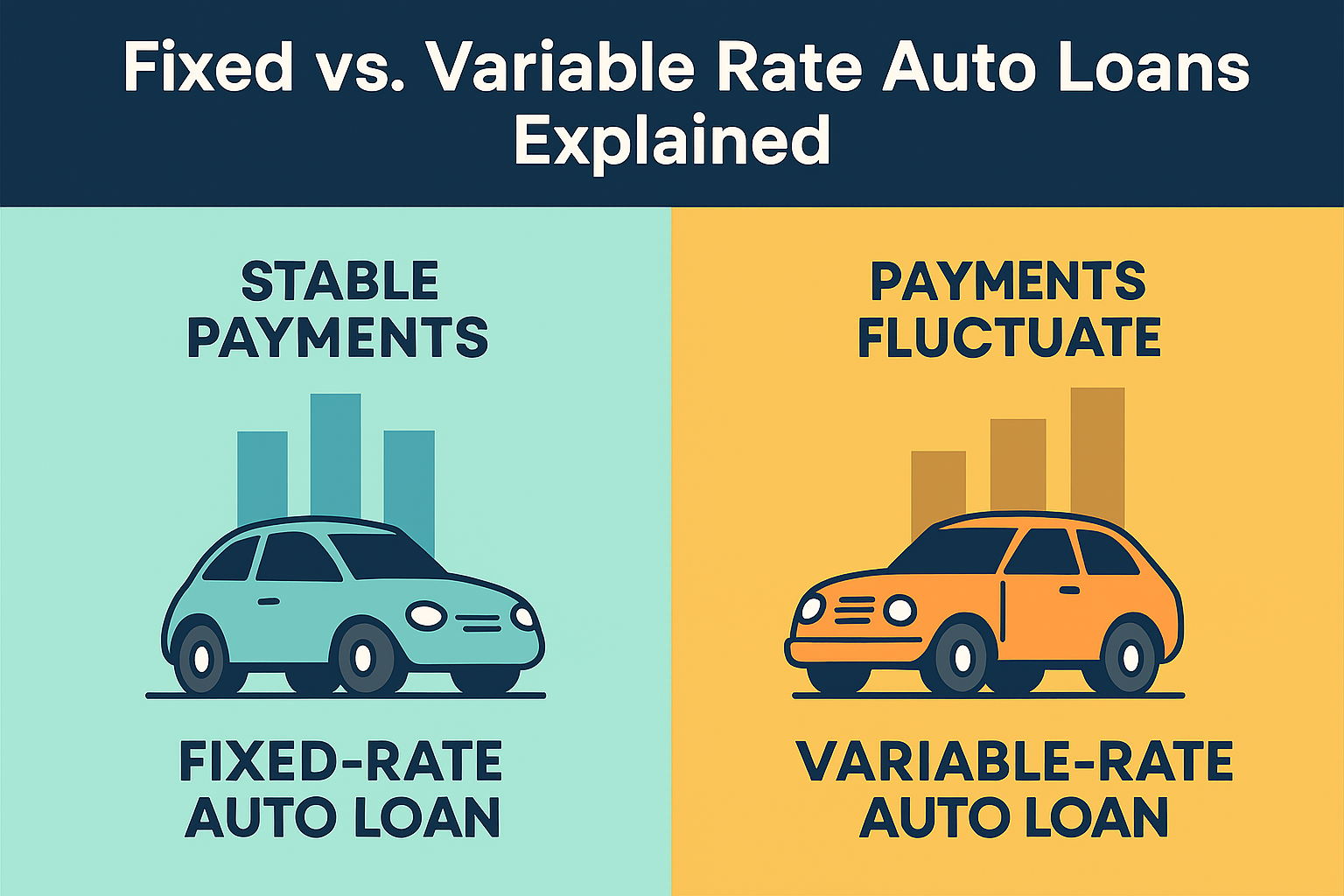

What Is a Fixed Rate Auto Loan?

A fixed rate auto loan locks in your interest rate for the entire duration of the loan. Your monthly payment stays the same from the first installment to the last. This consistency makes it easier to plan your budget and avoid surprises.

For example, if you borrow $25,000 at a fixed rate of 5 percent over 60 months, your monthly payment will remain constant. Even if national interest rates rise during that time, your rate and payment will not change.

What Is a Variable Rate Auto Loan?

A variable rate auto loan, sometimes called an adjustable rate loan, starts with an interest rate that can change over time. The rate is typically tied to a financial benchmark, such as the prime rate or another market index. As that benchmark moves, your loan’s interest rate may adjust at scheduled intervals.

These loans often begin with a lower introductory rate, which can make them appealing to borrowers looking for initial savings. However, if market rates increase, your monthly payment could rise as well.

How Different Loans Play Out

Instead of a side-by-side chart, let’s walk through how each loan type performs in real-world situations.

Scenario 1: Budget-Conscious Buyer with Long-Term Ownership

You plan to keep your car for at least five years and want to avoid any surprises in your monthly budget. You prefer knowing exactly what you’ll owe each month and are not interested in tracking market trends.

Best fit: Fixed rate loan. The stability of a locked-in rate ensures your payments never change, which supports long-term financial planning.

Scenario 2: Short-Term Owner with Strong Cash Flow

You expect to sell or trade in your vehicle within two to three years. You have a stable income and can handle moderate payment fluctuations. You’re also comfortable with some financial risk in exchange for a lower starting rate.

Best fit: Variable rate loan. The lower initial rate may save you money during the short time you hold the loan, especially if market rates remain stable.

Scenario 3: First-Time Buyer with Limited Credit History

You’re new to auto financing and want to avoid complexity. You’re focused on building credit and want a loan structure that’s easy to manage without worrying about rate changes.

Best fit: Fixed rate loan. The predictability helps you stay on track and avoid surprises while you build your financial profile.

Scenario 4: Rate Watcher with Refinancing Strategy

You’re comfortable monitoring interest rates and plan to refinance if market conditions shift. You’re open to a variable rate now but want the option to switch to a fixed rate later.

Best fit: Variable rate loan with a clear exit plan. Just make sure there are no prepayment penalties or refinance restrictions.

Pros and Cons

Fixed Rate Loans:

- Predictable monthly payments

- Easier to budget

- Protection from rising interest rates

- May start with a slightly higher rate

- Ideal for long-term ownership

Variable Rate Loans:

- Lower initial rate

- Potential savings if rates stay low

- Risk of payment increases

- Requires monitoring

- Better suited for short-term financing

How Market Conditions Influence Your Choice

Interest rate trends play a major role in deciding between fixed and variable loans. In a rising rate environment, fixed loans offer protection. In a stable or declining rate environment, variable loans may provide short-term savings.

Before choosing, review current economic forecasts and consider your personal financial outlook. If inflation is pushing rates upward, locking in a fixed rate now could save you money. If rates are expected to drop, a variable rate might offer more flexibility.

To compare current offers, explore our curated list of lenders offering the best auto rates based on credit tiers, loan terms, and vehicle types.

Questions to Ask Before You Decide

Before signing any loan agreement, ask your lender:

- Is the interest rate fixed or variable?

- If variable, how often does it adjust?

- What index is it tied to?

- Is there a cap on how high the rate can go?

- Are there prepayment penalties?

- Can I refinance later without fees?

These questions help you understand the full structure of the loan and avoid unexpected costs.

The choice between fixed and variable rate auto loans is not just about numbers. It’s about how much risk you’re willing to take, how long you plan to keep the vehicle, and how much flexibility you need in your monthly budget.

Fixed rate loans offer consistency and long-term clarity. Variable rate loans offer short-term savings with the possibility of future volatility. By understanding how each option works and evaluating your financial goals, you can choose a loan structure that supports your needs from day one to the final payment.

Frequently Asked Questions

How is a variable rate auto loan different from a fixed one? A fixed rate locks in for the entire loan term so your payment never changes, while a variable rate is tied to a benchmark like the prime rate and can adjust at scheduled intervals. Variable loans often start lower, but if the benchmark rises, your monthly payment can rise with it.

Who qualifies for or should consider a variable rate loan? It suits borrowers with strong, stable income who plan to sell or trade in the vehicle within two to three years and are comfortable with some payment fluctuation in exchange for a lower starting rate. If you are a first-time buyer building credit, a fixed rate is usually the safer, more predictable fit instead.

When does the timing of market rates matter most for this decision? In a rising rate environment, locking in a fixed rate now protects you from future increases, while in a stable or declining rate environment a variable rate may offer real short-term savings. Check current economic forecasts and your own ownership timeline before you commit either way.

What is a mistake to avoid with a variable rate loan? Signing on without asking how often the rate adjusts, what index it is tied to, whether there is a cap on how high it can go, and whether prepayment penalties exist. Skipping these questions means you could be caught off guard when your payment changes.

What if I take a variable rate now but want to switch to fixed later? That is a reasonable strategy if you plan to refinance when market conditions shift, but confirm there are no prepayment penalties or refinance restrictions in your current agreement first. Without that confirmation, an early payoff to refinance could cost you more than the savings you were chasing.

Leave a Reply