Your credit score plays a central role in determining the interest rate you’ll receive on an auto loan. It’s one of the first metrics lenders evaluate when assessing risk, and it directly influences how much you’ll pay over the life of the loan. Whether you’re buying new or used, financing through a bank or dealership, your score shapes the terms offered and the total cost of borrowing.

Understanding how credit scores affect auto loan rates can help you prepare strategically, compare offers more effectively, and avoid overpaying for financing.

What Lenders See in Your Credit Score

Your credit score is a numerical summary of your credit history. It reflects how reliably you’ve managed debt in the past and how likely you are to repay future obligations. Most lenders use FICO scores, which range from 300 to 850. The higher your score, the lower your perceived risk.

Key factors that influence your score include:

- Payment history

- Credit utilization

- Length of credit history

- Types of credit used

- Recent inquiries

Lenders use this score to assign you to a rate tier, which determines the interest rate range you qualify for. Borrowers with excellent scores receive the lowest rates, while those with lower scores may face higher costs or stricter loan conditions.

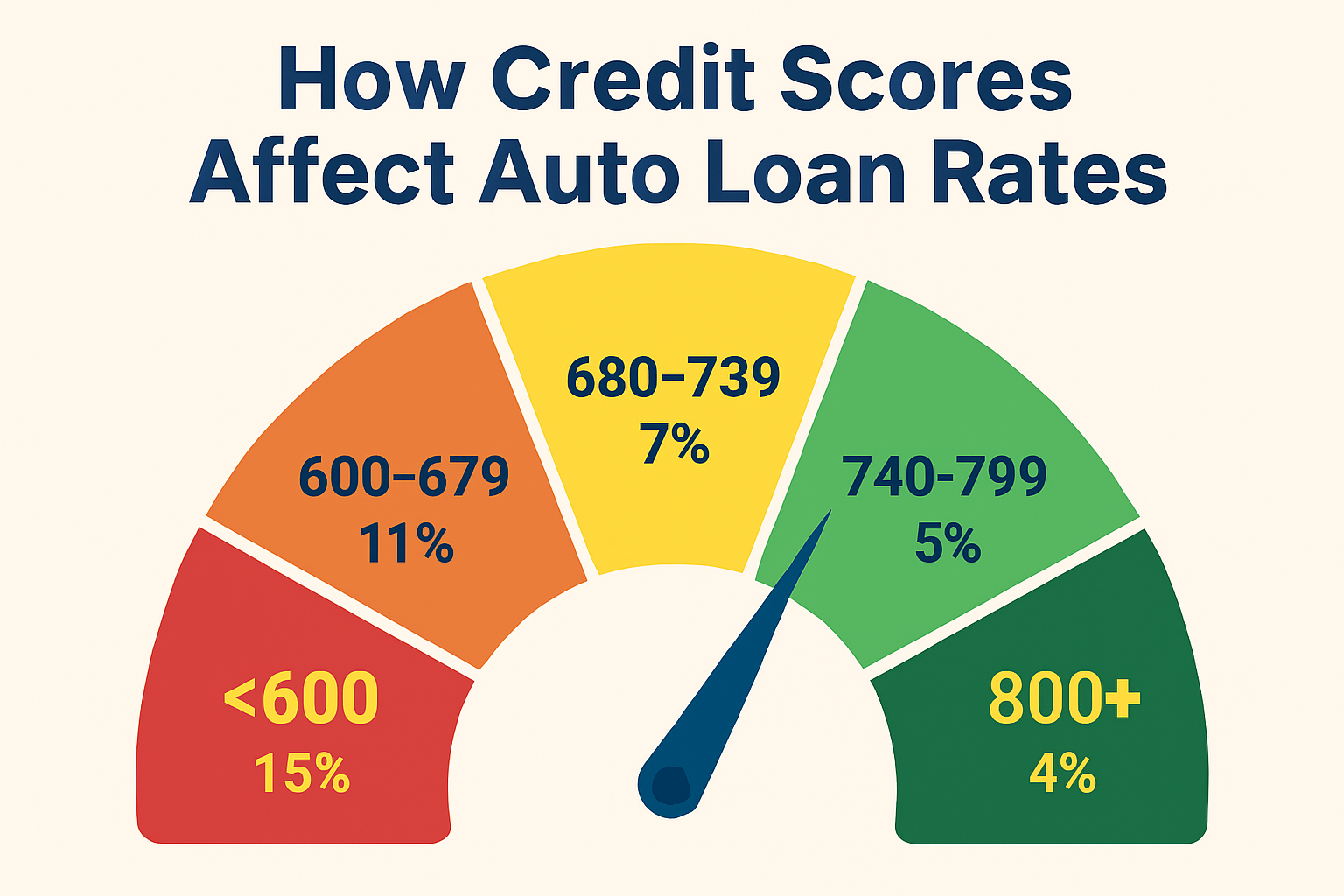

How Credit Score Affects Interest Rates

Auto loan rates vary significantly based on credit score. Here’s a general breakdown:

- Excellent (750–850) – Qualifies for the lowest rates available. These borrowers often receive promotional offers and flexible terms.

- Good (700–749) – Still eligible for competitive rates, though slightly higher than top-tier offers.

- Fair (640–699) – May face moderate interest rates and more limited lender options.

- Poor (below 640) – Higher rates, shorter terms, and stricter approval criteria. Some lenders may require a co-signer or larger down payment.

The difference between a 4 percent rate and a 9 percent rate on a $25,000 loan over 60 months can exceed $3,500 in interest. That gap reflects how lenders price risk based on your credit profile.

For a deeper look at how lenders group borrowers, see our rate tier explained guide, which breaks down how scores map to rate categories across banks, credit unions, and online lenders.

Why Rate Tiers Matter

Rate tiers are used to standardize pricing across different credit profiles. They help lenders manage risk and offer consistent terms to borrowers with similar scores. However, each lender defines its tiers slightly differently. One bank may consider 720 as top-tier, while another sets the cutoff at 740.

This variation means you should compare offers from multiple lenders. Even if your score places you in a certain tier, the actual rate offered can vary based on the lender’s underwriting model, loan term, and vehicle type.

Improving Your Score Before Applying

If your score is borderline or below prime, improving it before applying can lead to better rates and more favorable terms. Here are steps to consider:

- Pay down existing debt – Lowering your credit utilization ratio can boost your score quickly.

- Avoid late payments – Payment history is the most heavily weighted factor in most scoring models.

- Check your credit report – Look for errors, outdated accounts, or fraudulent activity. Dispute inaccuracies promptly.

- Avoid new credit inquiries – Each hard inquiry can lower your score slightly. Limit applications before seeking auto financing.

- Build positive history – If you have limited credit, consider a secured credit card or small installment loan to establish a stronger profile.

Even a 20-point increase can shift you into a better rate tier, saving you hundreds or thousands over the life of the loan.

Timing Your Application Strategically

Credit scores fluctuate based on activity. If you’re planning to apply for an auto loan, time your application when your score is at its strongest. Avoid applying immediately after a missed payment or large credit card charge.

Also, consider the timing of rate shopping. Most credit scoring models treat multiple auto loan inquiries within a short window (typically 14 to 45 days) as a single inquiry. This allows you to compare lenders without damaging your score.

How Loan Structure Interacts with Credit Score

Your credit score doesn’t just affect the interest rate. It also influences:

- Loan term length – Lower scores may result in shorter terms to reduce lender exposure.

- Down payment requirements – Higher-risk borrowers may be asked to contribute more upfront.

- Approval odds – Some lenders have minimum score thresholds. Falling below them may result in automatic denial.

- Refinancing options – A stronger score improves your ability to refinance later at better rates.

Understanding these interactions helps you structure your loan to match your financial profile and long-term goals.

What to Do If You Have a Low Score

If your score is below 640, you still have options. Consider:

- Working with credit unions or community banks – These institutions may offer more flexible underwriting.

- Exploring subprime lenders – Some specialize in working with lower-score borrowers, though rates may be higher.

- Using a co-signer: A co-signer with stronger credit can improve your approval odds and rate.

- Making a larger down payment – This reduces the loan amount and shows financial commitment.

- Choosing a less expensive vehicle – Lower loan amounts reduce lender risk and improve approval chances.

While rates may be higher, structuring the loan carefully can help you manage costs and improve your credit over time.

Your credit score is a key factor in auto loan pricing. It influences your interest rate, loan structure, and approval odds. By understanding how lenders interpret your score and how rate tiers work, you can approach financing with clarity and confidence.

Frequently Asked Questions

How much does my credit score actually affect my rate? A lot. The article gives an example where a $25,000 loan over 60 months can cost more than $3,500 more in interest at a 9 percent rate compared to a 4 percent rate, and that gap comes straight from how lenders price risk based on your score. Moving up a tier can save you real money.

What score do I need to qualify for the best rates? Aim for 750 or higher to land in the excellent tier, though 700 to 749 still gets you competitive offers. Below 640 you’ll likely face higher rates, shorter terms, and stricter approval criteria, and some lenders may ask for a co-signer or a bigger down payment.

When’s the best time to apply for an auto loan? Apply when your score is at its strongest, not right after a missed payment or a large credit card charge. If you’re shopping multiple lenders, do it within a 14 to 45 day window, since most scoring models treat those inquiries as a single pull instead of penalizing you for each one.

What’s a mistake people make when comparing rate tiers across lenders? Assuming every lender defines tiers the same way. One bank might treat 720 as top tier while another sets the cutoff at 740, so your actual quoted rate can vary between lenders even if your score qualifies you for the same tier on paper.

What if my score is below 640 right now? You still have options: credit unions and community banks often have more flexible underwriting, a co-signer with strong credit can improve your odds, and a larger down payment or less expensive vehicle reduces the lender’s risk. Rates will likely be higher, but structuring the loan carefully still helps you manage cost while you rebuild your score.

Leave a Reply